On maintaining the base rate at 18%

The Monetary Policy Committee of the National Bank of Kazakhstan has decided to set the base rate at 18% with a corridor of +/- 1 percentage point. The decision is based on the forecast round results, updated assessments of key macroeconomic indicators and inflation risks balance.

Annual inflation slowed down to 11.7% in February (12.2% in January) in line with forecast. Price growth is slowing across all inflation components. The food prices growth amounted to 12.7% (12.9%), non-food – 11.6% (11.7%), paid services – 10.8% (12%).

Disinflation is being supported by moderately tight monetary conditions, appreciation of the tenge, slowdown in unsecured consumer lending, reduction of excess liquidity through gradual increase of minimum reserve requirements and mirroring of gold purchases, comprehensive set of anti-inflationary measures implemented jointly with the Government. The moratorium on increase in prices for utilities and fuel contributes to the inflation decline as well. The impact of the VAT rate increase on inflation assessed limited.

At the same time, monthly inflation has accelerated and reached 1.1% in February 2026. The core inflation stood at 0.8%

Household inflation expectations one year ahead have decreased, but remain elevated and volatile (13.7% in February). February inflation expectations of professional market participants for 2026 have decreased to 10.0% (10.8% in January).

Global food prices continue to slow. Prices for dairy products and sugar continue to decline. Global prices increase has been recorded for cereals and vegetable oils.

Inflation remains elevated in Russia, the target is expected to be reached by 2027. The price growth in the European Union remains persistently low. In the United States the inflation is approaching its target under the US Federal Reserve calibrated policy.

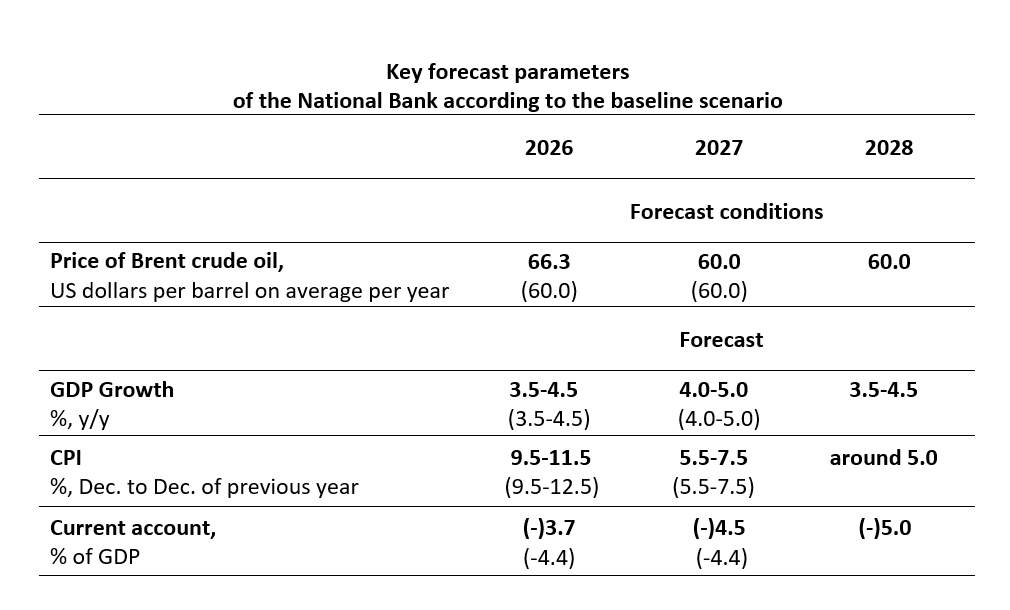

Under the baseline scenario, in the first half of the year Brent oil prices are projected to be temporarily higher than previously assumed, amid persistently elevated prices associated with the escalation of the conflict in the Middle East. Thereafter, oil prices are assumed to gradually decline to around USD 60 per barrel, based on the balance of global supply and demand. According to forecast, on average, it will amount to USD 66.3 per barrel in 2026 and stabilize at around USD 60 per barrel in the following years.

The inflation forecast for 2026 has been revised downward. Price growth is projected at 9.5-11.5% (previously 9.5-12.5%). Along with this, the National Bank expects the inflation to reach single-digit levels as a result of the implementation of joint actions by the Government and the National Bank, ensuring predictable fiscal and quasi-fiscal policies, as well as a reduction in the contribution of utilities and fuel prices to inflation growth. Inflation is projected to slow to 5.5%-7.5% by the end of 2027. By the end of 2028, it will be close to the 5% target.

Pro-inflationary risks have somewhat eased following the moderate price response to the VAT rate increase. Risks continue to be concentrated in domestic factors, including the effects of increases in regulated prices and elevated inflation expectations. The actual implementation of the planned budget consolidation in 2027-2028, as well as the scale and parameters of quasi-fiscal stimulus, also require attention. If transfers from the National Fund are not reduced as planned, the budget deficit does not decline, or quasi-fiscal stimulus expands without sufficient control, the disinflationary effect may weaken.

GDP growth forecast for 2026 remains in the range of 3.5-4.5%. A more balanced trajectory of economic activity in 2026 and further is expected due to the high base. Domestic demand is expected to slow amid fiscal consolidation and cooling consumer lending.

The National Bank will continue to assess the pace of inflation slowdown, the developments in domestic demand, the actual execution of fiscal consolidation measures, and the implementation quality of quasi-fiscal stimulus policies. The effectiveness of anti-inflationary measures will also be monitored jointly with the Government, along with developments in utility and fuel prices and the ongoing adaptation of households and businesses to the tax reform. Subject to a sustained slowdown in inflation and the absence of new pro-inflationary shocks, the possibility of the base rate cut will be considered from the second half of 2026. Under current conditions, the space for monetary policy easing has not yet developed.

More complete information about the factors of the decision and forecasts will be presented in the Monetary Policy Report on the official Internet resource of the National Bank[1] on March 11, 2026. The next planned base rate decision of the Monetary Policy Committee of the National Bank of the Republic of Kazakhstan will be announced on April 24, 2026 at 12:00 Astana time.

Detailed information for the media representatives is available upon request:

+7 (7172) 775 210

e-mail: press@nationalbank.kz

www.nationalbank.kz

[1] https://www.nationalbank.kz/ru/page/obzor-inflyacii-dkp