On maintaining the base rate at 18.0%

The Monetary Policy Committee of the National Bank of Kazakhstan has decided to maintain the base rate at 18.0% with a corridor of +/-1 percentage point. This decision is based on the results of the forecasting round, updated assessments of key macroeconomic indicators, and the balance of inflation risks.

Annual inflation in October stood at 12.6% (compared with 12.9% in September). Food price growth continued to accelerate, reaching 13.5% (from 12.7%), and non-food price growth rose to 11.0% (from 10.8%). Price growth in services slowed to 12.9% (from 15.3%) as a result of administrative reductions in regulated housing and utility tariffs. Elevated inflation dynamics are forming amid sustained demand that systematically exceeds supply capacity. Additional pressure stems from the continued transmission of second-round effects from tariff reforms and the liberalization of the fuel market into prices and inflation expectations.

The main contribution to inflation continues to come from the food component amid persistent imbalances in certain commodity markets, sustained demand, rising import costs, and higher production expenses. The contribution of service inflation has decreased but remains significant despite the slowdown in price growth. Within non-food inflation, an acceleration is observed in fuel prices and in prices for pharmaceutical products.

Monthly inflation slowed markedly in October to 0.5%, but core inflation remains high at 1%, which corresponds to 12.2% on an annualized basis. Furthermore, about 80% of goods and services in the consumer basket are experiencing price increases above the 5% target. All this indicates the persistence and broad scope of price pressures. This pro-inflationary dynamic is being reinforced by fiscal and expanding quasi-fiscal stimulus, as well as heightened consumer demand.

Inflation expectations among households increased in October to 13.6%, compared with 13.2% in September. Short-term expectations remain volatile and accompanied by high uncertainty. Long term expectations have risen to 14.3% (previously 14.0%). Elevated inflation expectations constrain the pace of disinflation and increase price sensitivity to changes in costs and demand.

External inflationary pressures persist. Global food prices remain at elevated levels. In Russia, despite the deceleration, inflation still significantly exceeds the 4% target. Against this background, the regulator maintains a firm rhetoric and signals the need to preserve restrictive monetary conditions. In turn, the Federal Reserve, amid heightened uncertainty, continues to take a cautious approach, noting moderate economic growth, a cooling labor market, and rising inflation, which remains above target. The European Central Bank’s rhetoric likewise remains restrained. The regulator has once again kept rates unchanged. Going forward, a more gradual pace of policy easing is expected.

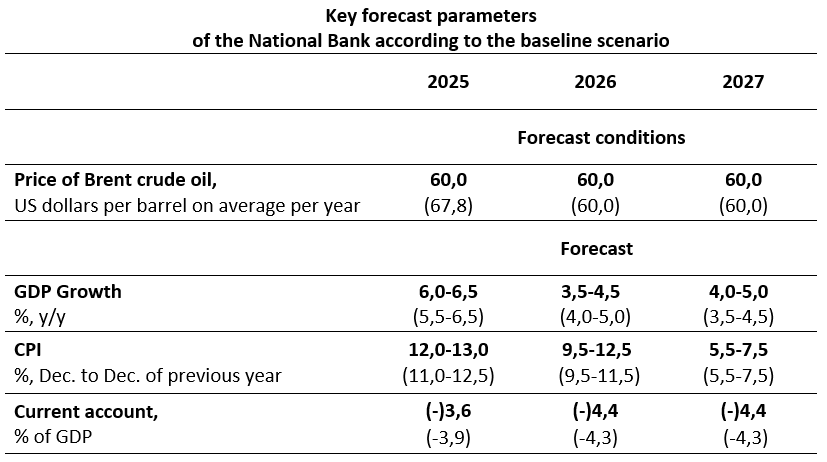

As part of the updated forecasts underpinning the policy decision, the Brent oil price in the baseline scenario has been maintained at USD 60 per barrel on average through the end of the forecast horizon.

The inflation forecast for 2025 and 2026 has been revised. Inflation in 2025 is expected in the range of 12.0–13.0%, and in 2026 within 9.5–12.5%. By the end of 2027, inflation is expected to slow to 5.5–7.5%. This revision is driven by the substantial overshoot of actual inflation relative to forecasts this year and by the elevated trajectory of inflation expectations. At the same time, the forecast revision also takes into account a more predictable increase in regulated prices, reflecting the revised pace of the reform carried out under the “inflation + 5%” scheme in 2026–2027.

The wider forecast range for 2026 reflects increased uncertainty in assessments related to the implementation of the tax reform and the response of aggregate demand, as well as the substantial increase in quasi-fiscal financing and its stimulative impact on the economy.

Disinflationary effects over the forecast horizon will be supported by a moderately tight monetary policy stance, fiscal consolidation, and measures implemented under the Joint Action Programme. Pro-inflationary effects will come from further liberalization of the fuel market and increased pressure from domestic demand driven by quasi-fiscal stimulus.

Forecast risks are associated with the intensification of imbalances between domestic demand and lagging supply, the acceleration of external inflation and inflation expectations, and second-round effects from increases in regulated prices, fuel prices, and VAT rate. A key source of uncertainty is the growing influence of increased financing to the economy by Baiterek National Managing Holding JSC (which, according to Government statements, is planned at 8 trillion tenge, equivalent to 4.4% of GDP in 2026), which may intensify inflationary pressures and partially offset the effect of the forthcoming fiscal consolidation.

The economic growth forecast for Kazakhstan for 2025 has been revised upward to 6.0–6.5%, reflecting the impact of faster growth in oil production, as well as an acceleration in investment and consumer demand in the final months of the year, partly driven by the upcoming VAT reform in 2026. The forecast for 2026 has been revised downward to 3.5–4.5% due to the high base of 2025 and the constraining effects of the fiscal reform and fiscal consolidation on domestic demand. In 2027, economic growth is projected in the range of 4.0–5.0%. The growth will be supported by continued growth in investment activity, moderate consumer demand, and higher oil production.

Strong domestic demand, amid declining real incomes and rising imports, increases the importance of coordination between fiscal and monetary policy. In this regard, the Government, the National Bank, and the Financial Regulation Agency are implementing the Joint Action Programme for Macroeconomic Stabilization and Welfare Enhancement for 2026–2028 (hereinafter – the Programme). The Programme is aimed at addressing imbalances between demand and supply, improving the efficiency of budget expenditures, implementing micro- and macroprudential measures, increasing real household incomes, and creating conditions for sustainable economic growth through reducing and stabilizing inflation.

Given the moderately tight nature of current monetary conditions, the expected contribution of the Programme, and measures to cool demand in consumer lending, the Committee’s decision aims to ensure a sustainable disinflationary trajectory.

The National Bank will continue to assess the pace of disinflation, the response of domestic demand, and the effectiveness of the coordinated measures implemented under the Programme and the Comprehensive Measures on Inflation Control and Reduction.

At present, the National Bank sees no room for rate cuts until the end of the first half of 2026, taking into account elevated inflation expectations, core inflation dynamics, and the delayed impact of tariff and tax reforms. In the absence of convincing evidence of a sustained disinflationary trend, the possibility of tightening monetary conditions cannot be ruled out.

More complete information about the factors of the decision and the forecasts will be presented in the Monetary Policy Report, to be published on the official website of the National Bank on December 3, 2025. The next planned decision of the Monetary Policy Committee of the National Bank of the Republic of Kazakhstan on the base rate will be announced on January 23, 2026 at 12:00 Astana time.

Detailed information for the media representatives is available upon request:

8 (7172) 77–52–10

e-mail: press@nationalbank.kz

www.nationalbank.kz