On maintaining the base rate at 16.5%

The Monetary Policy Committee of the National Bank of Kazakhstan has decided to maintain the base rate at 16.5% with a corridor of +/-1 percentage point. The decision is based on the outcome of the forecast round, which updated projections for key macroeconomic indicators and reassessed the balance of inflation risks.

In July, annual inflation remained at 11.8%. Food and non-food components continued to rise, while the services component slowed for the first time since the start of the year. As a result, the contribution of food products to annual inflation exceeded that of services, which had previously been the main driver. Inflation in paid services eased, in part reflecting slower growth in regulated prices.

Monthly inflation slowed to 0.7%, though it remains well above the historical average (0.4% for 2015-2024). Indicators of the underlying component of inflation also eased somewhat – core and seasonally adjusted inflation stood at 0.8% (compared with 0.9% and 1.0% in June, respectively). Despite the slowdown, their levels remain elevated and indicate persistent inflationary pressures, amid ongoing tariff reforms, fiscal stimulus, and sustained consumer demand, supported in part by strong growth in retail lending.

Household inflation expectations in July rose to 14.2%. Short-term expectations remain volatile, while long-term expectations show an upward trend.

External price pressures persist. Global food prices are rising. Inflation in Russia, despite slowing, remains high. The Federal Reserve’s rhetoric has softened somewhat, though external monetary conditions have worsened slightly compared with the previous forecast round in May, amid expectations of a slower pace of Fed rate cuts. This reflects inflation remaining above the Federal Reserve’s target, risks associated with US trade policy, and wage growth outpacing inflation. The European Central Bank’s rhetoric remains cautious, given the high uncertainty associated with trade conflicts.

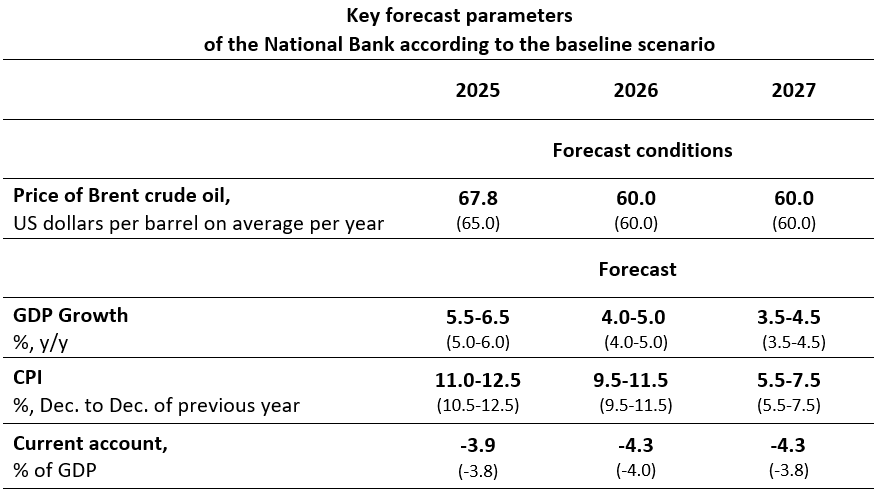

In updating the forecasts underpinning this decision, the Brent oil price in the baseline scenario was maintained at USD 60 per barrel on average through the forecast horizon.

The inflation forecast for 2025 has been revised. Medium-term projections remain unchanged. Inflation is expected at 11-12.5% in 2025, 9.5-11.5% in 2026, and 5.5-7.5% in 2027. The revision reflects price spikes in certain food markets and stronger pro-inflationary demand-side pressures. Moderately tight monetary policy and planned fiscal consolidation will have a restraining effect on inflation. Risks to the forecast stem from maintaining fiscal discipline, stronger domestic demand, an acceleration in external inflation, unanchored inflation expectations, and second-round effects from increases in regulated prices and VAT.

The economic growth forecast for Kazakhstan in 2025 has been raised to 5.5-6.5%. The revision reflects strong current growth momentum, high investment activity, and resilient consumer demand. The forecast for 2026 is maintained at 4-5%. Growth in 2026 will be supported by continued expansion in the oil sector and investment activity. From 2027, according to current forecast, GDP growth is projected to converge towards its equilibrium rate.

At its meeting, the Monetary Policy Committee also discussed additional measures that would help to reduce inflationary pressures. From September 2025, new minimum reserve requirements will take effect, strengthening policy transmission and thereby exerting additional disinflationary impact. Further practical steps will also be taken to improve the effectiveness of monetary policy implementation. The impact of existing measures is expected to be reinforced, together with the introduction of additional micro- and macroprudential measures aimed at cooling the retail lending market.

A failure to observe a significant slowdown in the pace of inflation in the coming months would provide grounds for tightening monetary conditions, in order to return inflation to a path of sustainable decline towards the medium-term target of 5%. On this basis, the Monetary Policy Committee will assess the appropriateness of raising the base rate at its upcoming meetings.

More detailed information on the factors behind today’s decision and the updated forecasts will be presented in the Monetary Policy Report, to be published on the official website of the National Bank[1] on September 3, 2025. The next scheduled decision of the Monetary Policy Committee of the National Bank of the Republic of Kazakhstan on the base rate will be announced on October 10, 2025 at 12:00 Astana time.

[1] https://www.nationalbank.kz/en/page/obzor-inflyacii-dkp

Detailed information for the media representatives is available upon request:

+7 (7172) 775 210

e-mail: press@nationalbank.kz

www.nationalbank.kz