On maintaining the base rate at 16.5%

The Monetary Policy Committee of the National Bank of Kazakhstan has decided to maintain the base rate at 16.5% with a corridor of +/-1 percentage point. The decision was made based on an analysis of the actual data, updated forecasts and an assessment of inflation risks balance.

In May, annual inflation reached 11.3%. The key driver of price growth in recent months remains service inflation due to significant increases in both regulated tariffs and market services prices. Acceleration in price growth is also observed for food products. Monthly inflation in May amounted to 0.9%, significantly exceeding historical dynamics. Core and seasonally adjusted inflation amounted to 10.1% and 11.4% respectively, in annual terms. All this indicates sustained price pressures amid renewed consumer demand growth, rising production costs, and ongoing fiscal stimulus. Inflation expectations among the population in May increased to 14.1% from 12.2% in April, indicating continued volatility and uncertainty regarding future inflation.

Pressure on prices from the external sector is intensifying. This is associated persistently high inflation in Russia, the continued rise in global food prices amid strong demand and currency fluctuations, as well as heightened uncertainty caused by escalating trade conflicts and volatility in commodity prices. Global price growth remains steady. Trade disputes are amplifying inflationary risks and constraining business activity in industry and services. Under these conditions, central banks maintain cautious rhetoric despite market expectations for further policy easing.

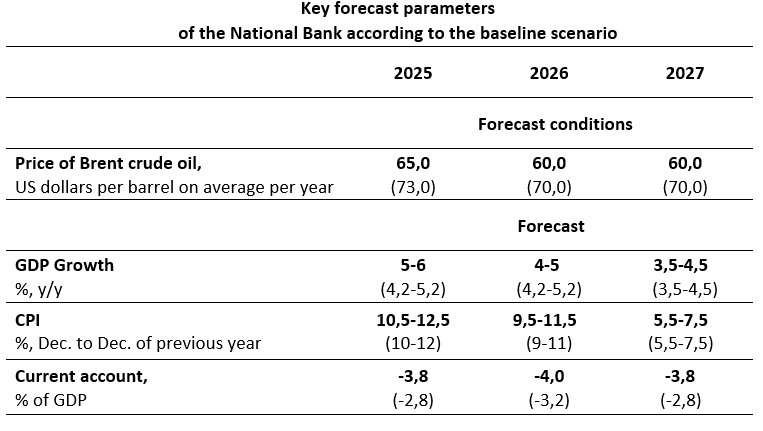

Under the baseline scenario, the price of Brent crude oil has been revised downward to an average of $60 per barrel until the end of the forecast period. Scenario conditions have been adjusted considering actual price dynamics and expected oil market supply exceeding demand.

The inflation forecast for 2025 and 2026 has been revised. In 2025, it is expected to be within 10.5-12.5%, in 2026 – 9.5-11.5%. By the end of 2027, inflation will decrease to 5.5–7.5% as a result of a restrictive monetary policy and gradual phasing out of budget support measures within the upcoming fiscal consolidation.

The upward revision of the inflation forecast for 2025–2026 is due to rising food prices, increased demand-side inflationary pressures, and lower oil prices. The main risks to the forecast include strengthening domestic demand, accelerating external inflation, and unanchored inflation expectations.

The ongoing moderately tight monetary policy and planned fiscal consolidation measures will continue to exert a restraining effect on inflation. At the same time, uncertainty remains regarding the actual rate of fuel price growth, the stringency of fiscal discipline (including the implementation of plans to reduce withdrawals from the National Fund), as well as the secondary effects of increases in regulated prices and VAT rates.

The economic growth forecast for Kazakhstan in 2025 has been raised to 5-6% due to stronger domestic demand and increased investment activity. The forecast for 2026 is 4–5%, considering stronger growth in 2025 and lower export growth due to the scenario of declining oil prices compared to the previous forecast. Economic growth in 2026 will continue to be supported by domestic demand and increased oil production. Subsequent growth will depend on the successful implementation of structural reforms planned by the Government, including measures to increase fixed capital investment, attract foreign direct investment, and liberalize the economy.

The evolving high inflation requires the maintenance of moderately tight monetary conditions for a longer period than previously expected. The balance of risks has shifted towards pro-inflation side, making it highly probable to keep the base rate at current level until the end of 2025. Maintaining the current policy stance aims to stabilize inflation expectations, prevent the consolidation of accelerating price growth trends, and return inflation to a sustainable downward trajectory toward the medium-term target of 5%. The National Bank does not rule out potential base rate increases if necessary.

As part of the expansion of its communication policy, the National Bank will begin publishing a summary of deliberations on base rate decisions starting from the current forecast round. This measure aligns with international practice and aims to enhance the transparency and predictability of monetary policy.

More complete information about the factors of the decision and forecasts will be presented in the Monetary Policy Report on the official Internet resource of the National Bank[1] on June 11, 2025. The next planned base rate decision of the Monetary Policy Committee of the National Bank of the Republic of Kazakhstan will be announced on July 11, 2025 at 12:00 Astana time.

[1] https://www.nationalbank.kz/ru/page/obzor-inflyacii-dkp

Detailed information for the media representatives is available upon request:

+7 (7172) 775 210

e-mail: press@nationalbank.kz

www.nationalbank.kz