Base rate maintained at 14.25%

The Monetary Policy Committee of the National Bank of the Republic of Kazakhstan has decided to maintain the base rate at 14.25% per annum with a corridor of +/- 1 percentage point.

Inflation increased slightly in July this year, yet it was within the forecasts of the National Bank. Monthly inflation and its stable part showed a significant acceleration. Inflation expectations of the population remain virtually unchanged after spike in June. Global inflation continues to slow down due to tight central bank policies in developed countries. The pro-inflationary pressure within the economy is increasing due to the growing volumes of fiscal stimulus, the continued increase in tariffs as part of the utilities reform, stable domestic demand, as well as increased inflation expectations.

Achieving the 5% inflation target in the medium term requires maintaining moderately tight monetary conditions for a longer time. The balance of risks has shifted to the pro-inflationary side which entails a high probability of maintaining the base rate at the current level until the end of 2024.

Annual inflation increased to 8.6% in July 2024, falling within the forecasts of the National Bank. The costs of regulated services continue to rise amidst implementation of the Tariff in Exchange for Investment program. The ongoing acceleration of inflation has occurred due to a significant increase in the cost of market services, rising production prices of the manufacturing industry and weakening of the exchange rate. At the same time, the dynamics of the decline in prices for agricultural products has weakened.

Monthly inflation increased to 0.7% in July, well above the historical average (0.3%). After stabilizing in the past months, the indicators of seasonally adjusted and core inflation have accelerated significantly, which signals an increase in the overall pro-inflationary pressure in the economy.

Inflation expectations of the population remained virtually unchanged in July. Respondents frequently note an increase in the cost of food, medicine and utility tariffs. Inflation expectations remain unstable.

Global inflation continues to slow down under restrictive monetary policies of leading central banks. Global food prices continued to decline in annual terms, but at a slower pace. In July, grain prices continued to decline conditioned by seasonal supply growth in the Northern Hemisphere and improved harvest expectations amid favorable weather conditions. Grain prices are expected to continue their gradual decrease.

External monetary conditions remain tight, but the stance of central banks has started softening. In particular, the US Federal Reserve, in view of successes in fighting inflation, signals the possibility of a rate cut in the near future. The ECB, having cut rates in June, is still determined to maintain tight monetary conditions because overall inflation is likely to remain above target in 2025. The Central Bank of Russia raised rates by 200 bps in July up to 18%, noting that significantly tighter monetary conditions are required for a period longer than previously expected to return inflation to the target.

Domestic aggregate monetary conditions have softened amidst weakening of the tenge exchange rate, acceleration of current inflation rates, and yet high annual growth rates of consumer loans.

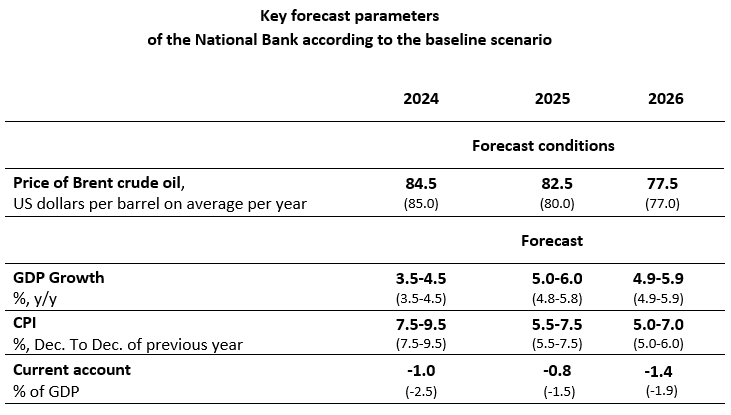

The baseline scenario of the forecast assumes stabilization of Brent crude oil prices at $84.5 per barrel on average in 2024 conditioned by the extension of OPEC+ production cuts, moderate production growth in the United States and geopolitical uncertainty in the Middle East. In the medium term, with increases in oil production and in consideration of forecasts for the development of the global economy, oil prices are expected to gradually decline to an average of $82.5 in 2025 and $77.5 in 2026.

The inflation forecast for 2024-2025 has been maintained in the range of 7.5-9.5% and 5.5-7.5%, respectively. In 2026, inflation is expected to reach 5-7%. The implementation of a moderately tight monetary policy will contribute to a slowdown in core inflation to 5% in 2026. At the same time, the uncertainties and risks of the inflation forecast are caused by an increase in fiscal stimulus against the background of a shortage of taxes and the implementation of large-scale government programs. Additionally, risks of the inflation forecast are associated with increased pressure from domestic demand, unanchored inflation expectations and acceleration of external inflation. Uncertainty about approaches and mechanisms to cover the increased gap between expenditures and revenues of the republican budget in 2024, as well as after 2025, poses a high risk. A further increase in fiscal momentum due to a shortage of taxes may trigger a revision of the National Bank's inflation forecasts.

The economic growth forecast for Kazakhstan in 2024 has been maintained at the level of 3.5-4.5%, for 2026 – in the range of 4.9-5.9%. The forecast for 2025 has been raised to 5-6%. GDP growth in 2024-2026 will be driven mainly by domestic demand together with increased fiscal stimulus. In 2025 and 2026, the oil sector will support economic growth as a result of increased production. According to the estimates of the National Bank, the economy will grow in conditions of expanding demand that surpasses supply during the forecast period. This will exert inflationary pressure.

Achieving the 5% inflation target in the medium term requires maintaining moderately tight monetary conditions for a long time. The balance of risks has shifted to the pro-inflationary side which entails a high probability of maintaining the base rate at the current level until the end of 2024.

The key parameters of the forecast are provided in the appendix. Detailed information on the determinants of the decision and forecast will be provided in the Monetary Policy Report on the official Internet resource of the National Bank on September 9th, 2024.

The next planned base rate decision of the Monetary Policy Committee of the National Bank of the Republic of Kazakhstan will be announced on October 11th, 2024 at 12 pm (Astana time).

Detailed information for the media representatives is available upon request:

+7 (7172) 77 52 10

e-mail: press@nationalbank.kz

www.nationalbank.kz

Appendix