Base rate reduced to 14.50%

The Monetary Policy Committee of the National Bank of Kazakhstan decreased the base rate by 25 basis points and has set it at 14.5% with a corridor of +/-1 percentage point.

Inflation decreased in April this year in line with the forecasts. There has been a slowdown in the stable part of inflation. Contrary to overall price dynamics, inflation expectations increased amidst floods and the ongoing reform of utility services. The external inflationary background is considered neutral, reflecting restrictive policies of foreign central banks and the dynamic of prices on world food markets. Pro-inflationary pressures within the economy are supported by ongoing fiscal stimulus, reforms in utility services and persistent domestic demand.

Achieving the 5% inflation target in the medium term requires maintaining a moderately tight monetary policy for a long time. A steady slowdown in the stable part of inflation shall create room for further cautious base rate cut. Current monetary conditions are aimed at consolidating the progress in decelerating inflationary processes and stabilizing inflationary expectations.

Annual inflation slowed to 8.7% in April 2024, which is in line with the forecast trajectory. There is a noticeable decrease in the food component of inflation conditioned by a favorable situation with external food prices. Likewise, non-food inflation subsided despite steady demand and increased consumer lending. Accelerated growth of costs of services was conditioned by growing utility prices.

Monthly inflation in April amounted to 0.6%, which parallels average historical figures (0.6%). The indicators of seasonally adjusted and core inflation have slowed down for the second month in a row. This is a result of a slower increase in food prices, while non-food and service components of the CPI remain above the target value.

Inflation expectations increased after two months of decline. According to respondents, this is conditioned by movements in food prices against the backdrop of a flood situation and the ongoing reform of utility services. At the same time, inflation expectations of professional financial market participants and enterprises are more stable, reflecting the trajectory of declining inflation and decelerating growth of prices for finished products.

The external inflationary environment is considered neutral. World prices for all types of foods except vegetable oils continue to decline in annual terms. External monetary conditions remain tight: both the Fed and the ECB have not yet eased monetary conditions and are keeping rates at restrictive levels. A slight increase of external inflationary pressure in the short term comes from Russia. However, considering the stance of the Central Bank of Russia on maintaining tight monetary conditions, a return to its target is expected by the end of 2025.

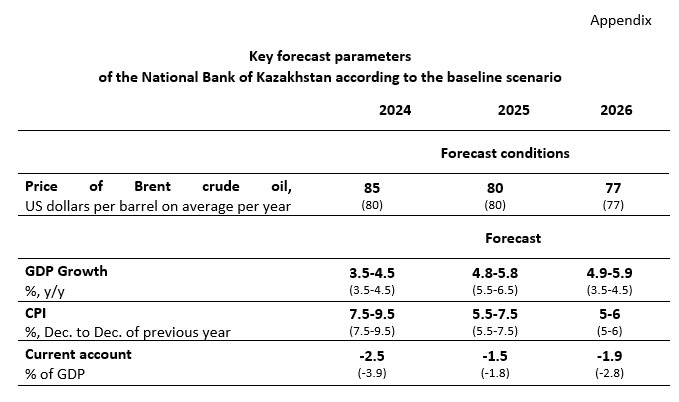

The baseline scenario assumes an upwards revision of Brent crude oil prices at 85 USD per barrel on average in 2024. This is conditioned by the extension of OPEC+ production cuts, stable production in the United States, and geopolitical uncertainty in the Middle East. In the medium term, with oil production increases and considering global economy development forecasts, a gradual scenario decline in oil prices is expected – to, on average, 80 USD in 2025 and to 77 USD in 2026. The scenario envisages a short-term increase in world grain prices until mid-2024 with a further gradual decline (FAO Cereal Price Index). Increased cereal prices in the current period are due to unfavorable weather conditions in Brazil and Russia.

The inflation forecast is maintained in the range of 7.5-9.5% in 2024 and within 5,5-7,5% in 2025. In 2026, as fiscal stimulus decreases and moderately tight monetary conditions become full-fledged, inflation will approach the target of 5% and develop in the range of 5-6%. The main risks of the inflation forecast are the uncertainty of fiscal policy parameters, the continuation of regulated price reforms, and increasing domestic demand pressures aligned with unanchored inflation expectations, as well as geopolitical tensions. At the same time, core inflation will be below headline inflation, forming at the level of 5% in 2025-2026.

Economic growth forecasts of Kazakhstan for 2024 has been maintained at 3.5-4.5%. Economic growth will be driven by consumer lending, investment activity in non-resource sector, and growth in real incomes of the population against the background of fiscal stimulus. Dynamics of tax collection and of the actual non-oil budget deficit indicate the continuation of a stimulating fiscal policy. Forecasts for 2025 and 2026 have been revised due to the postponed launch of the TCO expansion project, now expected in the second half of 2025. Outlook for 2025 has been reduced to 4.8-5.8%, for 2026 – increased to 4.9-5.9%.

Achieving the 5% inflation target in the medium term requires maintaining a moderately tight monetary policy for a longer period. A steady slowdown in the stable part of inflation shall create room for further cautious base rate reductions. Current monetary conditions are aimed at consolidating the progress in decelerating inflationary processes and stabilizing inflationary expectations.

The National Bank does not respond to the direct effects of the regulated prices reforms with rate hikes, but closely monitors the impact of secondary effects.

The key parameters of the forecast are provided in the appendix. Detailed information on the determinants of the decision and forecast will be provided in the Monetary Policy Report on the official Internet resource of the National Bank on June 10th, 2024.

The next planned base rate decision of the Monetary Policy Committee of the National Bank of the Republic of Kazakhstan will be announced on July 12th, 2024 at 12 pm (Astana time).

Detailed information for the media representatives is available upon request:

+7 (7172) 77 52 05